Overview of TDS

Tax deducted at source (TDS) is a tax that is deducted from income that a company in India pays to a recipient or supplier if the income amount exceeds a specific statutory limit in a financial year.

The types of income that are subject to TDS include:

- Salary.

- Interest and dividends.

- Winnings from the lottery.

- Insurance commission.

- Rent.

- Fees from professional and technical services.

- Payments to contractors and subcontractors.

The withholding amounts for TDS can be deducted from an invoice submitted by a supplier or from the payment that is issued to the recipient or supplier. Examples of recipients and suppliers include contractors, providers of professional services, employees, and real estate landlords. Companies submit a TDS certificate to each supplier on a monthly or yearly basis. The certificate includes the payments, as well as information about the company and supplier. Companies must also submit an annual return to the government for each recipient or supplier for the financial year. TDS certificate can be either Form 16 (R75I10A) or Form 26Q-P2P-IND (R75I122EQ). Form 16 is the TDS certificate which an individual submits and Form 26Q is the TDS certificate which a company submits to the tax authorities.

TDS must also be deducted from payments issued to third parties by both corporate and noncorporate entities. The entity must deposit the amount owed for withholding at any of the designated branches of banks that are authorized to collect taxes on behalf of the government of India. The entity must also submit the TDS returns, which contain details about the payments and the challan for the tax deposited to the Income Tax Department (ITD).

For electronic TDS, companies must generate the Form 26Q for each financial quarter. This is a statutory requirement for the ITD.

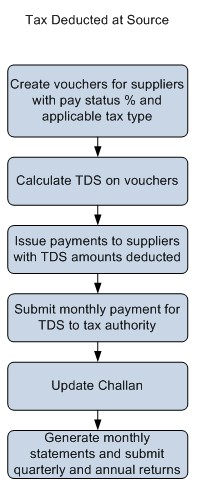

Process of TDS :

Or

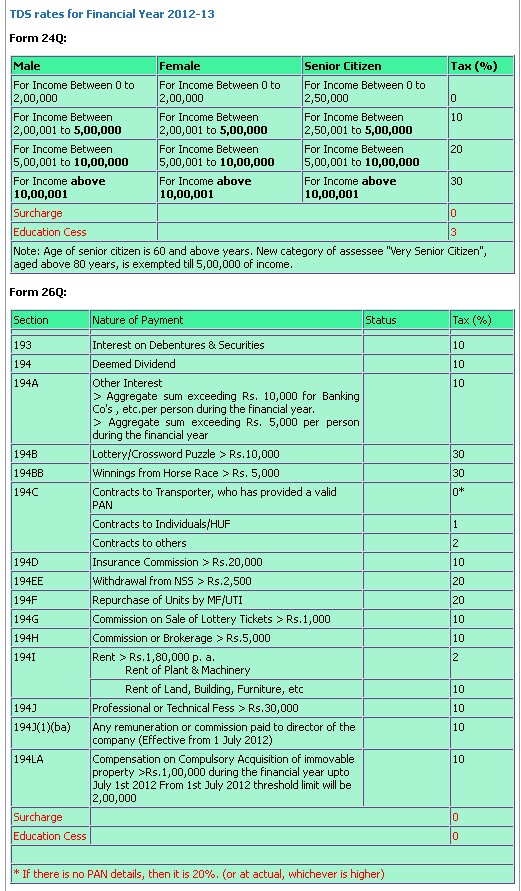

TDS/Withholding Tax Rates:

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.